Three Oil & Gas Names for Volatile Times in the Energy Sector

Source: Streetwise Reports 08/31/2017

With oil and gas prices not easy to predict, Samuel Pelaez, chief investment officer and portfolio manager of Galileo Funds, explains the algorithms that track "quantamentals," and discusses several companies that he expects to outperform.

The Energy Report: Sam, you employ what you call "quantamental" models. Would you explain what they are?

Samuel Pelaez: We've been developing these models for a number of years now and started using them across the board about two years ago. We started by looking at the stories where we'd been very successful and tried to identify what made them so special. We then tried to back into financial metrics that we could use to identify investments that would have the same potential to outperform the market.

The traditional value metrics are very powerful, especially for the gold and materials space, but you can't rely solely on a value factor or a growth factor. You have to develop multifactor models that give you enough exposure to protect yourself or to participate when the markets are going up or down. You have all these ingredients and the art is in how you put them together to create and end result that's very valuable.

In quantamental models, we use the fundamental data provided by the companies in their financial reporting. We try to take some of the data points and cross-reference them across the peer group or, in general, their industry, to identify which ones have a statistical difference that makes them stand out.

This process enforces a very high degree of discipline that I believe is generally absent when you don't have these very well-defined models. Anecdotally, the hardest thing with these models is not what to buy; it's actually when the model tells you that a specific investment is no longer good enough for your portfolio and you still believe it is. The discipline that it imposes on you in having to sell this position is actually very humbling. But that's part of the reason why we believe these models work, because they impose a very high degree of discipline on the money manager.

We actually use these models now for a number of funds. I have the benefit of running a global resources mandate, which is invested in a wide array of sectors and industries and also geographies. So, I've had first-hand experience over the last two years in identifying how these factors work in the materials space, specifically in gold versus the other materials, and then in energy, agriculture and infrastructure.

TER: What are some of the factors you consider?

SP: One of the most important factors is a high return on invested capital. This is one of the hardest factors for any one management team to influence. It measures management’s ability to deploy capital effectively over the longer term and as a result, it takes years for a management team to turn it.

We also look at enterprise value (EV); we don't look at market caps generally. It's a better comparable metric across industries and companies. EV relative to operating cash flows, free cash flows and on earnings before interest, tax, depreciation and amortization (EBITDA) gives a sense for the profitability of the company. Generally, the lower EV:EBITDAs, the lower EV:cash flows, tend to have better prospects.

One of the other metrics we have used across numerous industries and that we found is a pretty good indicator for future success is the efficiency of the management teams in terms of dollars. We measure that by the selling, general and administrative (SG&A) cost of the enterprise relative to the revenue it can generate. Across the board, we've seen companies that can deliver greater revenues to their SG&A have also, in general, higher margins, both at the gross margin level and at the EBITDA level. We believe that comes as part of the management team's approach to business; when they run a lean operation at the corporate office they are more likely to run a lean operation across the board, and that generally results in higher profitability ratios.

Perhaps the last one that we've seen that works across the board is the sales per share growth. The sales per share growth penalizes the companies that are serial issuers of shares irrespective of the returns that those investments would generate. We look at the sales per share growth over the last quarter over the four-quarter average to see if there's upside momentum in the revenue per share.

TER: These models were generated primarily for the gold and resource space. What happens when you transfer them to the energy space?

SP: We realized that the pure value factors, most of which I mentioned already, don't necessarily work by themselves in the energy sector. When we recognized that, we went on a very interesting study as to what were the key drivers of performance in the energy space. We came to a number of conclusions that have led us to explore other avenues in the rest of our models.

The first conclusion is the energy space is much more susceptible to momentum than the other sectors we track. That is both what we call fundamental momentum, which is the one quarter over four-quarter average growth, and also price momentum, which generally is not that good an indicator in many other sectors. But in the energy sector it is very powerful.

The second biggest lesson was that the large caps in the energy space behave very differently from the midcaps and the small caps. For example, large caps in the energy space are not very susceptible to value metrics, but they're highly susceptible to the sales per share growth. And they're very susceptible to the price momentum metrics. That is in contrast to the materials space, for example.

In the midcap energy universe, we found that those two momentum factors remained very strong, but if you add the value factors into a wider multifactor strategy, you get even better returns. In particular for the midcap universe, the return on invested capital is a very powerful factor.

The small-cap universe is the least susceptible to the momentum factors and is much more driven by value factors like the ones we've used in the materials space. So here is where you're looking at EV:EBITDA, EV:cash flow ratios, as well as the SG&A:revenue, to identify those companies with what we call the right culture where the management runs lean, profitability-based operations.

TER: Let's talk about some of the challenges from external factors that you've had with these quant models for energy.

SP: With energy being such a macro-driven market, there is a large number of exogenous variables that can affect the market regardless of the merits of our quantamental models. We recognize that, and we have a number of other models that track sentiment and momentum, not of the specific stock, but of the sector in relation to other sectors, of the commodity relative to other commodities and sectors, etc. We run correlations and causation studies that help us with that.

Perhaps most important is having a broad understanding of the macroeconomics and the politics at play at any time. We do that on our weekly writing of strengths, weaknesses, opportunities and threats (SWOT) models, which forces us to provide a balanced analysis.

The quantamental model is a bottom-up analysis, and SWOT is a top-down analysis. The quantamentals are very powerful at helping pick individual investments, but you need to have that overlay of the top-down macroeconomic and political assessment to recognize the exogenous forces at work.

TER: What are some of those forces?

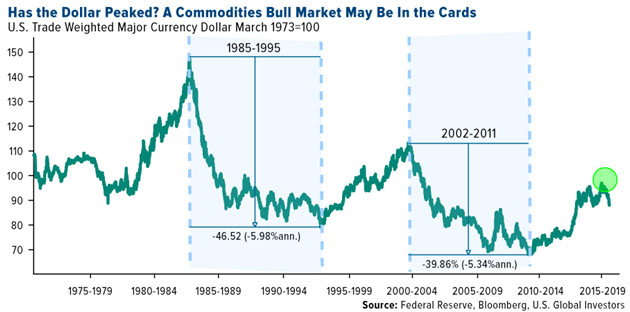

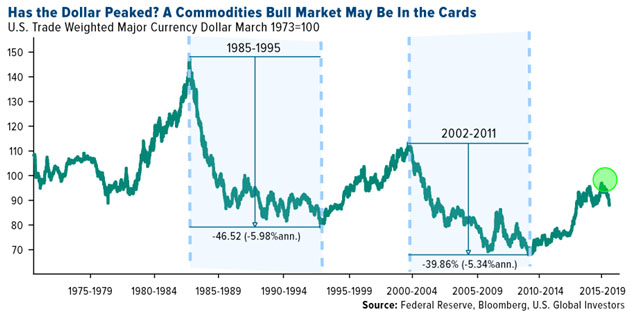

SP: I'll start with the strengths. The U.S. dollar has had one of its worst years in a good number of years. It's down more than 9% year-to-date despite the Federal Reserve rate hikes that have taken place. That's interesting because in the history of the Bloomberg Commodities Index, there's never been a year in which the dollar has been off more than 6% and the overall commodities have been negative for the year. Commodities as an asset class are negative this year, which means that based on past experience and that negative correlation of commodities to the dollar, one of them has to give. We believe what's going to happen is the commodities are going to rally, and especially crude has to recover from a year-to-date drop of over 12%.

There's a recent study that suggests that the U.S. dollar cycles are about 10 years in nature. If you look at the value of the dollar, the recent technical break on that chart suggests that twice in the past when we've seen that same break and what's ensued is a 10-year bear market on the dollar, which has coincided with rallying commodities and rallying emerging markets.

Has the dollar peaked?

If we see that, then we expect commodities in general, but especially energy, to be outperformers for the remainder of the year and actually into the next couple of years, which would be very positive for the whole sector. That weak dollar is one of the exciting parts of the market right now, and we really don't see strong evidence for a dollar recovery.

The main weakness right now, in my opinion, is the Organization of the Petroleum Exporting Countries (OPEC) cuts. Last November, OPEC entered into an agreement to curtail production across pretty much all of its members with some exceptions. It was very successful at first. It coincided with the election of Donald Trump as president of the United States. Energy prices rallied to about $50. It was a very exciting time.

What OPEC didn't account for was that the void that they were leaving behind in the market was going to be rapidly filled out by other participants, and those were the OPEC countries that were exempted from the cuts for various political and other reasons, like Iran, Libya and Nigeria, which have significantly increased their production over the last six months or so, and also non-OPEC producers, mainly the U.S. We've seen Permian Basin production recover quite dramatically, as has the rig count year to date. What's happened is that OPEC production was mainly replaced by production elsewhere.

The weakness now is Saudi Arabia and OPEC are sitting with this issue, which is how to communicate to the market that they are going to have to do away with these cuts and that some of that production may come back and perhaps we get an oversupplied market once again. I don't see a favorable outcome for this. Saudi Arabia has been suggesting that they're going to continue to cut exports, but any energy market specialist will tell you that over the summer, exports from Saudi Arabia tend to decline because its domestic consumption is significantly stronger owing to the weather. But those exports generally come back to the market in the fall. I think we need to wait and see what happens with that, I think it's in a tough spot right now.

Let me go over to the opportunities. This just came out of nowhere. The market reaction so far has been negative, but in my opinion, these have the potential to add a little bit of spice to the market here. Over the last couple of weeks, as companies in the U.S. have been reporting their quarterly earnings, we've started to learn that the rapid growth in rig count and activity and production out of the Permian Basin may be about to stall.

First there was Baker Hughes Inc. (BHI:NYSE), the big oil services company, which has warned that the inquiries for activity had been dropping and that it was attributing this to weaker prices. But it really didn't have a very clear explanation for it.

Then, Pioneer Natural Resources Co. (PXD:NYSE), which is one of the most active producers in the basin, reported earnings. The earnings were pretty good, but it downgraded the expectations or its guidance for full-year activity and drilling. Its explanation was that over the last couple of months, it has seen unreliable or unexpected changes on pressure at the wells it has been drilling.

If you fast forward, this means that the newest wells have become less economic. If this is something they can extrapolate to the whole basin, then perhaps further growth is not economic at these prices. So these companies are going to have to stop growing, the rig count is going to stall and production growth is going to stall. This has been the single largest driver for production growth in the U.S. year to date. If that stops, it sends a positive message to the whole market saying we cannot continue to grow at these prices. Fifty-dollar oil is not good enough or economic for us to continue that growth rate. That will be one of the biggest signals that the market has to start to rebalance, because one of the most prospective basins in the whole world can no longer grow at these prices.

Part of this is still speculation because this is one of the most recent developments in the energy space, but it's definitely something to track and to follow. It has the potential to change the landscape.

TER: Has this gone against the conventional wisdom of what the Permian Basin reserves are?

SP: Not as to what the reserves are, but perhaps the activity has ramped up so aggressively that it's just strained, growing too quickly, too fast. Pioneer has had to change the way it has been fracking the wells, and they become more expensive. The way these wells operate the cost is frontloaded, so it makes them less economic. Maybe some of the companies just stand back and say, well, it doesn't make sense for me to do it at $50 oil, so I'm going to just sit back and wait until prices go up. That should send a very positive signal for the global market because the Permian is indeed recognized as one of the best shale formations and one of the most productive ones.

TER: Let's go on to your last part of the SWOT analysis, threats.

SP: The purchasing managers index (PMI) trends have been weakening recently. We are big fans of tracking PMIs because they're one of the earliest macro indicators to be published every month. And they pack a lot of information in them. We've actually done numerous studies that suggest they actually have some predictive power. Specifically for the energy space globally, the U.S. PMI carries significant importance in that predictability, as does the Chinese PMI, although to a lesser extent.

We track the Institute for Supply Management PMI for the U.S. as the key leading indicator for energy. And that one has been disappointing in the most recent months after a good six- to nine-month run. That's one of the indicators we keep a close eye on. Right now, it's not particularly exciting. The Fed hikes should have a tightening effect on the U.S. economy. We're still not seeing any of the big political and infrastructure programs that were promised, so it's definitely a key indicator to keep an eye on in terms of it potentially getting weaker and its implications for energy.

As a wild card, I would mention the Venezuela situation. We've been tracking this for years. I was actually born in Colombia, and I have a good understanding of the political situation in Venezuela, which is a neighboring country. Markets have been following the news with particular interest over the last month or so even though the situation has been deteriorating for five years or longer. The reason for that is the recent referendum that is giving many more powers to the incumbent president. We have protests on the streets and the potential for some disruption. I believe that catalyst is real. I'm concerned as to what the timing of this catalyst may be because if you've been following the story, this could have come at any point in the last five years. And I'm not convinced, as other participants are, that it's going to come imminently.

This means two things: an opportunity and a threat. The opportunity is we see a major disruption for the global energy supply chain. The U.S. imports nearly a million barrels from Venezuela every day, especially to the Gulf refiners. Taking that million barrels off the U.S. imports on a daily basis would certainly have an impact on the global market.

This has more potential to be a threat than an opportunity, and that's perfectly exemplified by the case of Libya over the last number of years. Following a disruption there with the Arab Spring, it's added another degree of volatility to the energy market. The assets in Libya have been coming on and off the market, and that's created a lot of volatility for crude flows and prices. I believe that degree of volatility tends to be more damaging for the market than the potential benefit of having a disruption. So, it's definitely another key global issue to keep your eyes on and hopefully it will not be too disruptive to the overall market.

TER: Has Venezuela been able to keep its production fairly stable?

SP: Production has come off, but it's come off much less than initially expected. That has been partly because over the past decade it has been able to secure loans from other nations, mainly China. Now, as an aside, Venezuela pledged its oil reserves to China on these multibillion-dollar loans, which is also one of the reasons why I think there's not going to be an active political intervention from any of the Western powers, as we'd seen in other places. But that's just speculation on my end.

But production has been remarkably resilient. Venezuela still produces about 2 million barrels a day (2 MMbbl/day) when forecasts a number of years back were calling for those to drop to 1.5 MMbbl/day. That is because it has been able to skimp out on the capex and maintenance for its facilities. That generally doesn't bode well long term because my understanding is the facilities are severely impaired lacking major investment. We're not going to be seeing those flows of 2 million barrels (2 MMbbl) for much longer.

So I got back to my point where I say the catalyst is real. Venezuela is going to see a disruption. I'm just not sure when that takes place and how major it's going to be. I'm more worried about the volatility that it can bring into the market rather than the actual disruption.

TER: While we are speaking of threats, what longer-term effects do you think the damage inflicted by Hurricane Harvey will have on the market?

SP: I believe the effects of Harvey on oil prices have been exaggerated and we should see prices stabilize as the infrastructure returns to normal operation next week. The images of Houston are more striking than the actual damage on the infrastructure. So far none of the critical infrastructure has reported serious damage, so the ramp up to full capacity should be relatively quick.

TER: Let's move to companies. Given all of this analysis, what stocks look good to you right now?

SP: In the large-cap global integrated space, Royal Dutch Shell Plc (RDS.A:NYSE; RDS.B:NYSE) is our favorite among its peers. When we ran it through our quantamental models, it outperforms peers virtually in each of the factors that we find to be outperformers at this level. The sales per share momentum is far ahead of the peers. Our metrics show 9% versus 7% for the peer group. It also has superior efficiency ratios as measured by the SG&A:revenue. The dividends are also better covered than most of the peers at that level. The company has actually been paying back debt even though crude has been sub-$50. So it's been able to maintain a dividend without covering it with debt issuance. It's also been able to pay back the debt. Lastly, Shell has the best price momentum among the global integrated names.

I should warn investors and people interested in the stock that all of this—not just Shell but Total S.A. (TOT:NYSE), Chevron Corp. (CVX:NYSE), Shell, BP Plc (BP:NYSE; BP:LSE)—some of them are actually overbought on signals. This is one of the metrics we look at when trading the stock. So I wouldn't be a buyer right now. I'd wait for it to consolidate a little bit at this level or even drop 5% to the mid-low fifties before I added some exposure here.

Looking at U.S. producers, we do like Cabot Oil & Gas Corp. (COG:NYSE). This name has been somewhat neglected because of its gassy nature versus the oily nature of the Permian names that have been topical. But it has had some impressive sales per share growth momentum, ahead of all the names in the Permian and ahead of all of its peers in the Marcellus. It also has pretty strong efficiency ratios as measured by the SG&A:revenue. The return on capital, although not necessarily impressive on an absolute basis, does rank in the top decile of all the U.S. exploration and production companies. In addition, the company has some sizable growth opportunities in front of it. It has a strong balance sheet and all the other traditional things you would look for in a good investment.

TER: How about in the small-cap and junior market?

SP: For the small caps, there's a company that recently went public on the Canadian market. It's called Pentanova Energy Corp. (PNO:TSX.V). Even though it just acquired some producing assets as well as some development assets, we don't have official numbers. But we've run our pro-forma models on what the company will look like once it reports earnings. We have confidence that is this going to be one of the names that will meet our models and will outperform. The market cap is just CA$75 million. That's give or take $60 million enterprise value as the company has cash.

Two of the company's assets will be operating assets. All of these assets are in Colombia and Argentina, which, as you know, is an up and coming, powerful energy prospect. One of these assets is called Llancanello. It's owned by Yacimientos Petrolíferos Fiscales (YPF:NYSE), which is a state-owned company in Argentina, and Pentanova is earning up to 50% in this project. This is a producing asset in which the Pentanova team is going to apply its expertise. The people at Pentanova come from previous successes like Parex Resources Inc. (PXT:TSX.V), Pacific Rubiales and PetroAndina, all of which have been successful in Colombia and Argentina, and they have a very strong technical background. They're bringing this technical background to drill and expand production of this asset. They believe they can grow this asset from 8 Mbbl/day to 40 Mbbl/day in three years.

Pentanova will own 50% of that. If you assume 20 Mbbl and the EV of CA$60 million, the return on capital is pretty amazing. But just with more traditional metrics that people are used to, you will be paying about CA$3,000 per flowing barrel. That's on an EV basis. And on a market cap basis, you're paying probably CA$4,000 per flowing barrel. Just for context, in Canada you pay CA$50,000 on average for listed peers; you pay 10 times more for a flowing barrel of oil. In the U.S., especially in the Permian, you pay CA$70,000. This company is trading at $0.10 on the dollar effectively when you look at these numbers. This is just on one of its assets. It has, I believe, five more assets in Argentina and Colombia, which have similar high return on capital prospectivity.

TER: Any final thoughts that you'd like to express?

SP: Generally, I like to tell readers that forecasting the price of oil consistently is possibly the hardest thing in the world of investing. There are specialists trying to do this every day, and it's nearly impossible to do it on a consistent basis. What we've done with these quantamental models is create a framework for us to select investments that have the right ingredients and the potential to outperform on both markets, when oil prices are going up and when oil prices are going down. That's the beauty of the quantamental models, that you can back-test these strategies across rising markets and falling markets, and you can study the anatomy of the selection process. We're very confident that we've been able to identify the right factors and the right mix of such factors to deliver alpha.

I would encourage investors to think long term and stand behind and support good stories with good management teams and good return on invested capital. Then you don't have to worry about whether the price of oil is going to $60 or to $45. You can sleep well at night and know that you're handing over your capital to people who know what they're doing and they're doing it as efficiently as they can.

TER: Thanks for your time, Sam.

Samuel Pelaez is chief investment officer and portfolio manager with Galileo Global Equity Advisors. Prior to that he was an investment analyst at U.S. Global Investors, a boutique U.S.-based investment management firm. Mr. Pelaez graduated from the Schulich School of Business with Distinction in 2012. He also holds a Masters in Finance degree from The University of Cambridge. He is a CFA charter holder and member of the Toronto CFA Society.

Want to read more Energy Report interviews like this? Sign up at www.streetwisereports.com/get-news for our free e-newsletter, and you'll learn when new articles and interviews have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Articles page.

Disclosure:1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Samuel Pelaez: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I, or members of my immediate household or family, are paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this interview: None. Funds controlled by Galileo Funds own securities of the following companies mentioned in this article: Pentanova Energy Corp. (PNO:TSX.V). I determined which companies would be included in this article based on my research and understanding of the sector. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Connect with us on Facebook and Twitter!

Follow @EnergyNewsBlog