Which Energy Companies Are Being Added to US Global Funds in Anticipation of an Oil Rebalance?

Source: JT Long of The Energy

Report (1/26/16)

There are still winners in the energy space, but you have to

move quickly. In advance of the rebalance U.S. Global Investors CEO Frank

Holmes is expecting toward the end of 2016, he and analyst Samuel Pelaez point

to the sectors taking advantage of opportunities, including refiners, midstream

MLPs, low-cost producers, airlines and chemical companies. In this interview

with The Energy

Report, they name their favorites and outline the fundamentals that

will make 2016 look a lot different than the year that just ended.

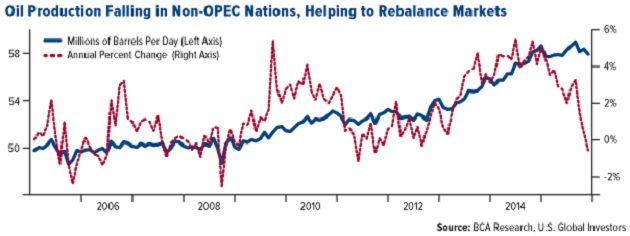

The Energy Report: In a recent Frank Talk, you quoted BCA Research with

a prediction that oil markets will rebalance in 2016. What is that based on?

Samuel Pelaez: This chart shows that the U.S. has come off its peak

production quite a bit. We reached peak production in April at about 9.6

million barrels (9.6 MMbbl). We're about 400 thousand barrels (400 Mbbl) off

from that level. This goes a long way to rebalancing the supply/demand dynamics

globally. Even though the U.S. has been a major contributor to rebalancing the

supply in the markets, we have not seen the supply come off to the levels we

were initially expecting. We thought about 1.2 MMbbl could be curtailed, but

only managed to get about 400 Mbbl.

One reason for the continued

production is that banks are pressuring explorers and producers (E&Ps) to

bring in cash flow. The only way for these companies to bring in more cash flow

is to continue growing production, or at least maintaining production. On top

of that, we've seen massive efficiency gains in shale productivity. So even

though the rig count has fallen dramatically, the U.S. has been able to sustain

production at a relatively good level, which actually bodes really well going

forward, from a U.S. supply perspective.

Now, what really needs to change for

a supply/demand rebalance is for OPEC's volumes to stabilize. Toward the end of

the year we saw that even though the U.S. was cutting production, OPEC

production grew. In November, during their last meeting of the year, they

unofficially abandoned their quota system, which they had brought from 30.5

MMbbl all the way up to 31.5 MMbbl. We saw 700 Mbbl of increased production

come in toward the end of the year, which more than offset the U.S. supply

volume. So even though we think supply is going the right way and OPEC's

boosted production may not be sustainable, we believe we're coming to that

point where supply will continue to erode gradually as a result of low oil

prices.

More interestingly, on the demand

side of the equation, China, the largest oil consumer, actually imported a

record amount of oil in December, a total of 7.8 MMbbl of oil equivalent a day.

That's 16% growth month over month. It is clearly taking advantage of lower oil

prices, and we expect that dynamic to continue going forward. The lower oil

prices resulted in dramatic increases in gasoline consumption around the world.

More importantly, China is expanding its strategic oil reserves to take

advantage of this window of opportunity, which gives you a sense that it

doesn't think it is sustainable going forward.

Purchasing Managers Indexes (PMIs)

are the best leading indicator for commodity demand, especially in China. As of

now, global PMIs—including China PMIs—are in a negative downtrend. That means

that the one-month number is below the three-month trend. Until that changes,

we don't expect a significant price recovery. However, as we go into the summer

peak driving season and the peak oil demand season, we expect inventory draws.

We've seen massive inventory build-ups. We may see that turnaround. That will

make us more comfortable that prices have bottomed, supply growth will start

outpacing demand growth and we will slowly and gradually move toward a

rebalanced market toward the end of the year.

TER: Do your supply side calculations include Iran? What impact

could that have when it starts shipping oil again?

SP: It's actually very hard to forecast OPEC supply. But we do

expect to see Iran volumes increase since sanctions were lifted. Iran has said

it is ready to increase production by about 500 Mbbl. We think that is

realistic. It believes it can grow to 1 MMbbl, which essentially will take it

to pre-sanction level. We don't expect it to go above that, considering the

lack of investment over the past few years and that major significant

investments will be required for Iran to be able to grow production back up to

4 MMbbl per day (4MMbbl/d). So yes, we do expect that to be a significant

driver in terms of volumes earlier in the year; however, we don't expect that

to fully materialize. There are both upsides and downsides to this because it's

very hard to estimate what the market is pricing in, but we believe in Q1/16

and perhaps all the way until seasonal factors kick in during Q2/16 we'll

continue to see pressure on the prices down.

TER: Do you agree, Frank?

Frank Holmes: I do. I think that the pivot point is going to be the

Federal Reserve trying to mitigate financial-meltdown bank lending in the

energy patch. That could change the guidelines for asset sales. I think what's

going to happen is we're going to get a bottoming, we're going to see supply

drop and we're going to see all future funding for a lot of these operations

come to an end, which will fast track this contraction in the energy supply in

the U.S.

I also think Iran is a real threat.

Costs are so much lower there. In the short term, money can be made meeting

Iran's technology needs. In fact, it needs Boeing Co. (BA:NYSE) planes. It

needs parts. It needs all the necessary chemicals and upgraded drilling equipment

for the energy space. So there will be many companies that are going to

benefit, but that will still put pressure on energy prices.

TER: Another thing that's changing is that after years of

restrictions, the ban on exporting oil from the U.S. has been lifted. How much

of an impact could that have on oil prices?

FH: More supply. If energy is to spike, then America will make

that trade-off very quickly from supplying domestic chemical companies to

exporting to higher price markets.

SP: I think more than the overall impact to global oil prices,

it achieves a more globally efficient allocation of the resources. That would

benefit American producers because the U.S. has nearly doubled its oil

production in the last five years, but most of it is in the ultralight

condensate space. Those are volumes that refiners in the States don't need. But

Mexico could use for its gasoline. This allows producers to sell product

internationally without a discount. We had West Texas Intermediate (WTI)

discounts for the longest time, I think up to $30 relative to Brent, and it was

because of the abundance of this condensate and light crude oil in the US. It

was great for refiners at the time. Now, producers will be able to get better

international prices relative to Brent. That is why we saw that WTI-Brent

spread collapse. Overall, I think it benefits everybody in the States.

I have heard some criticism about

consumer gasoline prices rising as a result. That is simply not true because

there has never been a ban on exports of gasoline, only on raw products. The

U.S. has always had gasoline prices that are commensurate with international

markets. In that regard, it doesn't change anything.

TER: When I interviewed Chen Lin recently, he was hoping for $20 a barrel ($20/bbl)

oil because he said that would lead to a faster jump back up in price. We

dipped below $30/bbl recently. How many oil and gas juniors can survive to see

that upside if Chen is right?

SP: I absolutely agree with him. Although we don't hope for

prices to continue to collapse, the lower prices go, the more pain is inflicted

and the quicker the supply responds from swing producers, especially tight oil,

which is the more expensive kind of oil.

The Wall Street Journal published a piece recently saying that E&Ps are losing

$2 billion ($2B) a week at $30/bbl oil. That's just in the U.S. Even though

marginal cost curves, which is something we look at frequently, are now pointing

at about $25/bbl globally for that marginal barrel of oil, it ignores all the

capex, the general and administrative (G&A) expense, the debt servicing,

etc. So I struggle to believe that there are many companies making money at

these prices. They can continue to pump out some production, the ones that have

already been established, but there will be no new supply additions at these

prices.

FH: The currency also impacts it. If you're an American

producer, you're much more severely impacted by oil prices falling because your

costs are in dollars. However, if you're in Canada, the currency has declined

so much that you're still able to marginally stay in the game as a player. The

same thing happens with Colombia. The currency declines have been so severe for

some of these countries that companies operating there can survive even with

these low energy prices.

TER: How many oil and gas juniors are still in your portfolio?

How do you decide who to keep?

SP: We have reviewed the juniors in our portfolio and we remain

committed to a narrow number of companies, specifically those with proven

management that have been able to demonstrate their ability to be first movers

into key growth areas.

One of those names is BNK

Petroleum Inc. (BKX:TSX). It has one of the best assets in all of Oklahoma.

It has continued to beat everybody's estimates in terms of the decline rates.

It has been able to squeeze more oil out of every well in this play than

anybody ever predicted. Those are the kinds of plays we like. We like those big

growth opportunities with proven management. It also has come a long way in

cutting costs. I think its G&A was cut by 50% year over year. We see great

optionality for the ability to grow going forward. It will need a little bit of

a better price just like everybody else, but we're comfortable holding it today

because the cost adjustments it has been able to implement will allow it to

survive this trough.

FH: I know some oil companies that have cut their Houston

office, but have added people in Calgary because their currency has declined so

much. So the cost of intellectual capital, seismic research, etc. is a lot

cheaper there for an international oil company. BNK originally came out of

Calgary, so its cost structure has declined because of the Canadian dollar.

TER: How are the majors shifting their focus to take advantage

of global opportunities? What role do they play in a diversified energy

portfolio?

SP: By definition, the integrated majors are the best way to

ride a storm. They've traditionally been the defensive names in the space, and

they continue to be so. If you look at last year's performance, they massively

outperformed the energy sector. That's even before you factor in the dividends,

which are obviously much more sustainable. The role they play is critical, and

it changes over time. But I think at this juncture, when we're expecting even

lower equity returns, dividends and share repurchases become a big and important

part of your returns.

We prefer American versus European

majors. The U.S. majors have a much greater exposure to profitable downstream

sectors. The U.S. downstream sector as a whole is more profitable than the

European one, owing to greater gasoline demand, overall better crack spreads,

better margins and overall profitability.

We look for majors that are focusing

on extracting the most profitability out of their downstream space right now in

order to continue to sustain their dividend growth. I think this is the big

driver of the valuations of these companies. We look for those that have strong

free cash flow yields, robust balance sheets, sustainable dividends and a focus

on the downstream space.

We own Exxon

Mobil Corp. (XOM:NYSE). The company has positioned itself as the best major

to weather the storm. We see a number of major integrateds repositioning their

portfolios in light of the price collapse, but we think Exxon was way ahead in

doing this and the downstream exposure will allow it to weather the storm

better than most of its peers. It will also become more active in the mergers

and acquisitions space once it recovers.

TER: Are there still opportunities in the midstream space? Do

they have less exposure to price risk?

SP: Absolutely. This is especially true after 2015. Master

limited partnerships (MLPs) and midstream as a whole was the worst performing

subsector in the energy space last year. That is because there's this investor

view within the MLP space of "one size fits all." This couldn't be

further from the truth. Investors argued that MLPs and midstreams will see

falling dividend growth as a result of lower volumes and expected supply cuts.

As we've seen, the supply cuts did materialize, but not to the extent that was

initially thought. Also, the rate hike had a big effect on the underperformance

of MLPs, but now we know that further rate hikes are not so clear in coming in

the future. As I mentioned earlier, yields and dividends become a more

important portion of your return this year. Building on that, I think within

the MLP space we have a lot of pockets of value. I wouldn't recommend the

sector as a whole, but I would recommend those MLPs whose toplines have the

least correlation to oil prices. Some of them have great exposure to volumes

from shale plays that continue to grow even at current prices. Those who

participate in that specific space and have robust balance sheets will be able

to sustain their payout rates, and those yields will become very important this

year.

We particularly like a company

called EQT

Midstream Partners LP (EQM:NYSE). This is a midstream company with pipelines

and storage capacities in the Marcellus. It has a very robust balance sheet and

low debt relative to its peers. It has a top-tier growth profile, posting a 40%

growth trailing 12 months. It also has one of the highest cash flow returns in

invested capital in the space. We expect it to continue to grow, especially as

it expands to the Utica Formation, and continue to pay about a 4% dividend

yield, which is very sustainable considering it's only a 60% payout rate. More

importantly, EQT is highly insulated from declines in volumes because it

operates more like a utility in the sense that it contracts out its capacity

ahead of time to producers, so it's not subject to the stock changes in

volumes. This also provides greater visibility into its revenue, into its

earnings and into the sustainability and eventual growth of its dividend.

TER: What are the prospects for the refiners in this scenario?

What companies do you like in that space?

FH: It is important to ask who is going to benefit from cheaper

gas besides the consumer at the gas pump. There are so many manufacturing

companies that are experiencing expanding margins because their energy input is

a big part of their costs. Refineries definitely benefit, but so do chemical

companies.

SP: The fundamentals for refiners are very basic. Input costs

are coming down as crude prices come down whereas their output, which is mainly

gasoline and distillates, is priced off of a mix of demand and cost. So they're

insulated on the cost side, and actually gasoline demand posted a record last

year. This results in fatter margins, which drives profitability, dividend

payouts, share buyback programs and overall great stock performance.

Record gasoline demand in 2015 is

expected to continue into 2016, resulting in strong double-digit crack spreads

in January, one of the weakest seasonal periods. This is incredibly favorable

for refiner markets. Ironically, the refiners sold off into the first two weeks

of the year, kind of mimicking what they did last year when the seasonality

kicked in, but that only set them up for 2015 when they were the best

performing sector within the energy space.

A few companies are poised to profit

from the upcoming spring turnaround season and are better able to profit from

this tightening in the supply, leading into the best oil and gasoline demand

season, which is the summer.

In light of that, we like Valero

Energy Corp. (VLO:NYSE), here in San Antonio. It has the best free cash

flow yield in the sector at 9%. That's 50% above the average for its peers.

This is a result of its complex system that allows it to take multiple kinds of

crude. It can go out and shop for the cheapest and extract very good products

out of pretty much any of them. It also has a large scale, and most of the

exposure is in the Gulf, which offers more access to cheaper product and, thus,

expanded margins. We expect it to continue to grow its dividend and the share

repurchase programs. We have this as one of the core holdings in our portfolio.

[Editor's note: Valero raised its dividend by 20% on Thursday after the

interview was conducted.]

We also like Marathon

Petroleum Corp. (MPC:NYSE). It has one of the strongest growth rates in the

industry. Although it has significant capital commitments, we've seen in the

past that the cash flow return on invested capital is one of the highest in the

energy space. That speaks to the capital discipline. It's actually a great time

to be building something because the energy sector is in a downturn, meaning

there is a lot of labor available, a lot of contracting equipment and a lot of

willingness to see these things through. It is exposed to this cyclical

tailwind.

We also like Tesoro

Corp. (TSO:NYSE). Even though it is not in the Gulf, we're still

comfortable sacrificing some of that exposure as a trade-off to the present

profitability and growth that it's been able to get out of the California

refineries. California is the biggest gasoline consumer in the U.S. Tesoro has

a prime location to benefit from that.

On the chemicals side, input costs

for Dow

Chemical Co. (DOW:NYSE), LyondellBasell

Industries NV (LYB:NYSE) and other diversified chemical companies are

directly priced off of crude. So you normally see them selling off with the

whole energy space when in fact what's selling off is their input. Their output

is sold to consumers, packagers, paint companies and a bunch of other

industries that use their chemicals. But this plays to the same dynamic that we

like in the refiners and in the integrateds. It's that further downstream

exposure, being closer to the consumer and a little bit more distant from the

prime commodity where we've seen much of the carnage. That's the reason we like

the chemicals, too.

TER: So there are some winners still in the space.

FH: Yes, and a big part is how fast you move to see if there

are tipping points for energy prices that trigger bankruptcies. I think you're

going to get a lot of bankruptcies this quarter and writedowns of reserves.

It's another reason why there will be a drop in supply as the industry goes

through this contraction. Any time you've had a commodity down for 36 months,

it will trigger a resetting of reserves and impact loan repayment.

The airline industry is another

industry that's had a big windfall from dropping energy prices to the tune of

expansion that this past year was $20B of additional free cash flow. With oil

at $30/bbl, this industry will probably push close to $35B of free cash flow

this year.

TER: Our readers are used to investing in junior mining

companies that can have really big wins. How can they get that same bang for

their buck in companies as large as the airlines?

FH: The airlines are pretty volatile. In fact, they have the

same DNA of volatility as junior mining stocks. They are going to go through a

rerating soon. Everyone expected them to undercut each other, and they didn't.

Instead, they started buying back their stock. I think that these airlines will

benefit from that.

TER: What final words of advice do you have for investors

looking at their portfolios in the wake of a volatile first few weeks of the

year and a rough three years?

FH: We have always been advocates of 5% bullion and 5% actively

managed gold mining companies like our World Precious Minerals Fund. When we

come to individual names, we've always stuck with Franco-Nevada

Corp. (FNV:TSX; FNV:NYSE) because it's a high-margin business and it

invests in a lot of juniors, so you get that portfolio.

Roger Gibson, a pension fund

consult, advocated back in 1997 that investors keep 25% in resources and

rebalance each year. He lost a lot of his customers, but they all came back in

2003 after the tech collapse because they recognized his wisdom. I agree with

his advice, but you need smart people like Sam on active management to take

advantage of a changing market like this.

SP: Even in the current price environment, there are numerous

opportunities to profit within the energy space. We discussed a number of

downstream exposure opportunities. They're all beneficiaries within the further

energy complex of lower crude prices. We feel like some investors are

apprehensive to take on some of these opportunities because some of them played

out last year, but that doesn't necessarily mean they can't play out again this

year. We look for a confluence of factors in terms of supply and demand to tell

us the market has changed, and we have not yet gotten to that point. We want to

see supply curtailments materializing, whether it's in the U.S. or OPEC. We

also want to see demand growth from China and the rest of the world that is

confirmed by PMIs crossing one month above the three-month, so that we can feel

confident that the trend has changed. Until that happens, we feel confident in

recommending the downstream exposure.

TER: Thank you both for your time.

Frank Holmes is CEO and chief investment officer at U.S.

Global Investors Inc., which manages a diversified family of mutual funds and

hedge funds specializing in natural resources, emerging markets and gold and

precious metals. Holmes purchased a controlling interest in U.S. Global

Investors in 1989 and became the firm's chief investment officer in 1999. Under

his guidance, the company's funds have received numerous awards and honors

including more than two dozen Lipper Fund Awards and certificates. In 2006,

Holmes was selected mining fund manager of the year by the Mining Journal. He

is also the co-author of "The Goldwatcher: Demystifying Gold

Investing." He is also a regular commentator on the financial television

networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune,

Barron's, The Financial Times and other publications.

Samuel Pelaez is an investment analyst covering global

resources. He joined Galileo Global Equity Advisors in 2015 after having worked

as an investment analyst at U.S. Global Investors, a boutique U.S.-based

investment management firm. Samuel graduated from the University of Cambridge

in the UK with a Masters in Finance, having previously graduated from the

Schulich School of Business (with Distinction) in Toronto, Canada. Samuel has

passed all three levels of the CFA program and will be eligible for award of

the CFA charter upon completion of the required work experience.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles

have been published. To see a list of recent interviews with industry analysts

and commentators, visit our Interviews page.

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: none.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: BNK Petroleum Inc. Franco-Nevada Corp. is not affiliated with Streetwise Reports. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Frank Holmes: I own, or my family owns, shares of the following companies mentioned in this interview: None outside the portfolio. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: USGI held these names in one or more funds as of 12/31/15: BNK Petroleum Inc., Exxon Mobil Corp, Tesoro Corp, Marathon Petroleum Corp, Valero Energy Corp. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Samuel Pelaez: I own, or my family owns, shares of the following companies mentioned in this interview: None outside the portfolio. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

5) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

6) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

7) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: none.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: BNK Petroleum Inc. Franco-Nevada Corp. is not affiliated with Streetwise Reports. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Frank Holmes: I own, or my family owns, shares of the following companies mentioned in this interview: None outside the portfolio. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: USGI held these names in one or more funds as of 12/31/15: BNK Petroleum Inc., Exxon Mobil Corp, Tesoro Corp, Marathon Petroleum Corp, Valero Energy Corp. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Samuel Pelaez: I own, or my family owns, shares of the following companies mentioned in this interview: None outside the portfolio. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

5) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

6) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

7) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

Streetwise

– The Energy Report is Copyright ©

2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC

hereby grants an unrestricted license to use or disseminate this copyrighted

material (i) only in whole (and always including this disclaimer), but (ii)

never in part.

Streetwise

Reports LLC does not guarantee the accuracy or thoroughness of the information

reported.

Streetwise

Reports LLC receives a fee from companies that are listed on the home page in

the In This Issue section. Their sponsor pages may be considered advertising

for the purposes of 18 U.S.C. 1734.

Participating

companies provide the logos used in The

Energy Report. These logos are trademarks and are the property of the

individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Petaluma, CA 94952

Tel.: (707) 981-8204

Fax: (707) 981-8998

Email: jluther@streetwisereports.com

Fax: (707) 981-8998

Email: jluther@streetwisereports.com

Connect with us on Facebook and Twitter!

Follow @EnergyNewsBlog